The Astute Angle tackles a question that we commonly receive in conversations with clients. The question comes in many forms but often resembles the following:

I have an emergency reserve (or cash stored up for a future home/car/asset purchase) that I want to keep safe but I also want to make a little return on this money. How should this reserve be invested?

First things first: when it comes to this kind of reserve, we strongly advocate that you divorce the concept of investing and gravitate towards the concept of preservation. Your emergency reserve should not make you rich. It should not even make you affluent. It should not be locked up. The primary objective is to do no harm.

Thinking liquid and safe means that investments such as real estate investment trusts (REITs), high yield bond funds, and diversified stock funds should be categorically avoided for such a purpose. Imagine you had $100,000 set aside for the down payment on a home next month and you purchased high yield bonds or high dividend stocks in September 2008 to try to squeeze out a little more return over the next 30 days. Merely a month later, your $100,000 was worth somewhere in the neighborhood of $75,000.

We even advise against using high grade bonds or bond funds for an emergency reserve in almost all cases because the limited upside doesn’t adequately compensate for the potential short-term losses. Such investments may yield 2% to 4% in today’s environment – better than what can be earned from your average savings account or money market fund. The problem is that while such investments (including US Treasury bonds) may be relatively safe from default, they are not immune from significant losses if interest rates increase. It would not take an extreme interest rate move for such bonds or bund funds to lose more than 10% of their value in a short time. This is clearly not ideal if you’re depending on the reserve for a near-term purchase or simply to provide peace of mind.

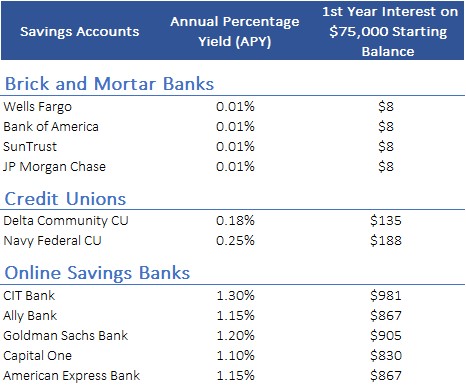

Our long-standing advice for an emergency reserve or short-term savings is a high yield savings account from one of the established online banks. A thorough list of these options and rates can be found here or here. Why trouble with such accounts rather than a traditional brick and mortar bank savings account or even a credit union savings account? In most cases, the online savings accounts have no fees, minimum deposits of $1, are FDIC insured to $250,000 per account (or $500,000 for a joint account), can be established in 5-10 minutes, are immediately available for withdrawal, and provide dramatically better interest rates than the savings accounts of brand-name brick and mortar banks. Consider the current annual percentage yields (APY) for a $75,000 savings account at several institutions¹:

It should be clear that the online savings banks are far more consumer friendly than the traditional banks. And who couldn’t use an extra $800 – $1,000 each year?

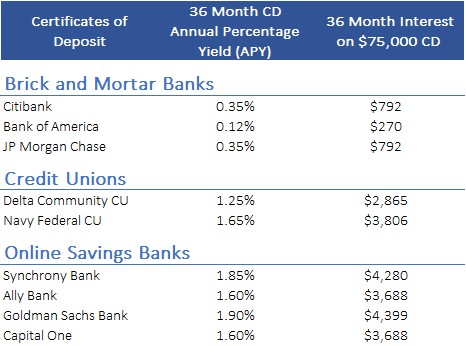

Another good option we occasionally recommend is a CD from one of these same online savings accounts. There are advantages and disadvantages. The clear advantage is the higher interest rate. At Goldman Sachs Bank, for example, you make 1.3% on the traditional savings account and 1.9% on a 3-year CD. The drawback of the CD is availability to funds. If you need the funds during the term of the CD, you can liquidate at any time but you face an early termination penalty that varies by bank.

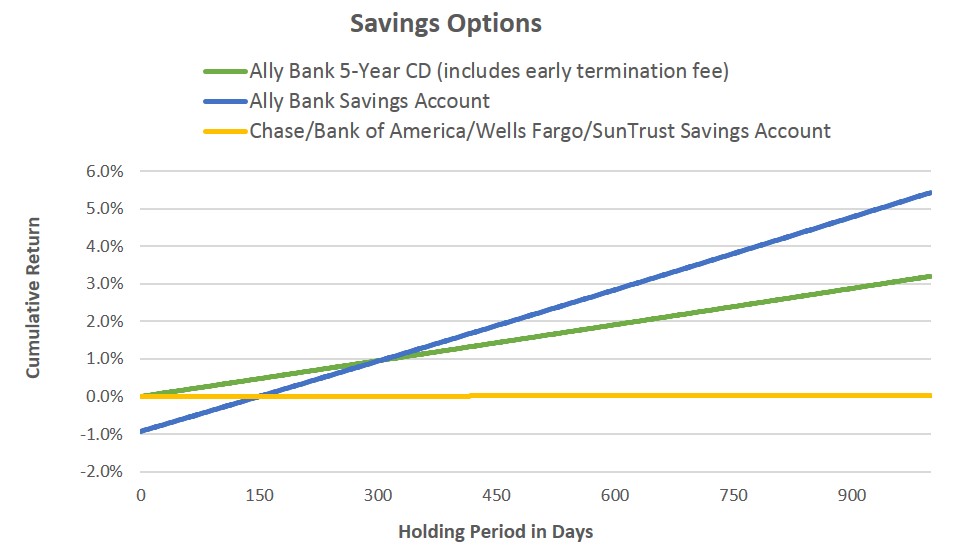

We often recommend 2-5 year certificates of deposit (CDs) for savings when there is no imminent known cash need and the funds are serving strictly as an emergency reserve. In fact, buying a CD can provide a better return in many cases, even if you end up needing the funds before the CD matures. The chart below compares one of the more flexible 5-year CDs from Ally Bank (150 days interest penalty for early exit compared with 250 days to a year of interest for most CDs) to other savings options. After 151 days, the CD provides a higher total return than the brick and mortar bank savings accounts where many people hold their cash – even when factoring in the early exit fee on the CD. Hold the cash for at least 304 days, pay the exit fee, and you’re still better off using the 5-year CD than the 1.15% Ally Bank savings account.²

Closing Thoughts

Two mistakes are commonly made when it comes to setting aside reserve cash and both mistakes are at the extremes. One extreme is taking additional risk to try to squeeze out a slightly higher return. It is parking cash in a high yield bond fund that provides a 4.5% yield and thinking that yield and/or the principal are safe. While this might be a reasonable position to own in a diversified long-term portfolio, it is inappropriate for a cash reserve. The problem is that you face being a forced seller at an inopportune time.

The other extreme mistake is letting a cash reserve sit in a savings account from one of the brick and mortar banks that earns approximately nothing. Inertia – the tendency to do nothing or to remain unchanged – is a powerful force. It is the reason why many consumers leave 5- and 6-figure cash reserves sitting in zero yield bank accounts or parked in CDs from those same institutions earning a fraction of what they could be earning in consumer-friendly products from consumer-friendly institutions. Our advice if you are making this mistake? Stop trying to figure out how you can save $5 on that next Amazon purchase and, instead, spend 10 minutes opening a high yield savings account or purchasing a CD with one of the consumer-friendly savings banks. It will likely be among the most economically profitable 10 minutes of your year.

¹APY rates are current as of 8/11/2017 and come from Mybanktracker, Bankrate, and Nerdwallet.

²This math assumes that the rates on the savings accounts stay fixed for the entire period. If, for example, the rate on the Ally Bank savings account increases during the period, then the 304-day breakeven period is longer. If the opposite happens and the Ally Bank savings yield drops during the period, the 304-day breakeven period becomes shorter.

Leave A Comment