An important issue that often arises for working professionals seeking to save for retirement is whether to utilize a Traditional 401(k) or Roth 401(k) for retirement savings. Although this dilemma may seem utterly confusing and resultantly receive less thought than the decision of whether to accept an old co-worker’s Facebook friend request, it can have a dramatic financial impact (good or bad). Unfortunately, many people saving for retirement fail to evaluate the Roth vs. Traditional 401(k) retirement options in terms of their situation or, because of a lack of education, are simply not aware that they even have a Roth 401(k) plan option.

What is a Roth 401(k)?

The Roth 401(k) (officially, the “Designated Roth Account”) is a recent innovation in retirement planning. It originally launched in 2001 under EGTRRA but failed to gain any meaningful adoption until 2006 when the Pension Protection Act made the Roth 401(k) permanent and removed earlier sunset provisions. According to data from Vanguard Group, 42% of employers with a 401(k) plan began offering the Roth 401(k) option by 2010. As of 2015, 56% of employers offer a Roth 401(k) option and the numbers continue to grow. Yet while the Roth 401(k) has steadily gained adoption by employers, data indicates that only 14% of participants able to use a Roth 401(k) are doing so.

From a tax perspective, Roth 401(k) accounts behave the same as Roth IRAs. An employee defers after-tax salary to the Roth account and the savings in that account grow tax-free, forever. Alternatively, the Traditional 401(k) (like the Traditional IRA) allows employees to save pre-tax dollars and defer taxation on the income and any future gains until the time at which funds are distributed.

Should I Use the Roth 401(k) or Traditional 401(k)?

Like with most financial planning decisions, the answer depends on a person’s unique circumstances. With that important caveat in mind, we can present a basic framework for evaluating the decision without the assistance of a tailored analysis.

Young, Early-Career Professionals

The answer to this Roth or Traditional 401(k) dilemma tends to be easiest to answer for young, early-career professionals. Importantly, the economics of a Roth account work best when you have one or both of two things: 1) a lower personal tax rate now than your expected future rate; and 2) time. Young professionals tend to have both. They clearly have time until retirement for the tax-free compounding effects of the Roth to materialize. Additionally, many young professionals in the early part of their career find themselves with lower income and, subsequently, in a lower tax bracket relative to their expected future income and tax bracket. The clearest example of this is a medical student in residency who may expect to see income increase by a factor of 10 in the future.

For these reasons, the economics tend to overwhelmingly support young professionals in their 20’s and 30’s using the Roth 401(k) for all retirement deferrals.

Mid-Career Professionals Not Currently Maximizing Retirement Plan Deferrals

Employees under age 50 are limited to $18,000 in annual contributions to a 401(k) plan (combined between any combination of Roth and Traditional deferrals). Employees over age 50 have a $24,000 limit. Most successful professional families will not be able to save enough for retirement with just 401(k) plan deferrals but there still may be years when a mid-career professional family is paying college tuition bills, has reduced income, or faces unusually large expenses, that they may not have the financial ability to reach these deferral limits.

With this in mind, consider a corporate executive who is stretched thin in the current tax year and estimates an ability to save $10,000 to a Traditional 401(k). The evaluation here is not whether she should contribute $10,000 to a Roth or $10,000 to a Traditional 401(k). If we assume that she is in a 40% combined tax bracket, the Traditional 401(k) contribution effectively reduces her take-home income by $6,000 ($10,000 contribution minus 40% or $4,000 of tax savings). Alternatively, a Roth 401(k) contribution of $10,000 would reduce her take-home income by the full $10,000 since there are no immediate tax deductions.

As a result, the evaluation here is whether to contribute $10,000 to a Traditional 401(k) or $6,000 to a Roth 401(k) since this is an apples to apples comparison as far as take-home pay is concerned. The reality is that if the professional in this example can only afford to contribute $10,000 to a Traditional 401(k), then she cannot legitimately afford a $10,000 Roth contribution.

What should she do? If the inability to reach the deferral limits is the result of reduced income, then the Roth 401(k) tends to be the best choice for reasons we address here. That is, if the executive in our example is limited because her income this year is atypically low, she should defer $6,000 to the Roth 401(k). Alternatively, if her income is high but unusual expenses are the reason that she cannot reach the deferral limit, the $10,000 Traditional 401(k) deferral is likely her best choice.

Mid-Career Professionals Currently Maximizing Retirement Plan Deferrals

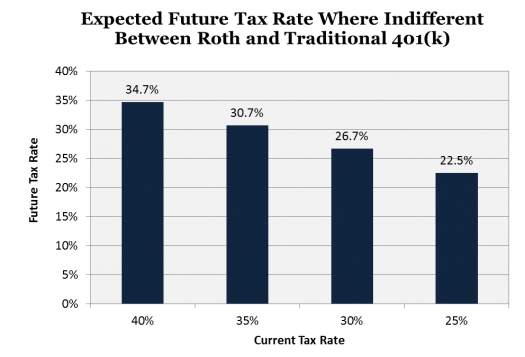

For professionals who are able to maximize 401(k) plan deferrals, the Roth vs. Traditional evaluation is impacted by time horizon, portfolio expected return, and portfolio tax efficiency but essentially boils down to the current tax rate versus the expected future tax rate at the time funds will be withdrawn.

Rule of thumb financial advice on the subject of Roth or Traditional contributions tends to suggest that people who are in a high tax rate now and expect to be in a lower tax rate in the future should use a Traditional IRA or 401(k). The idea is that you can deduct contributions now when you’re benefiting from the tax deduction at a high tax rate and then withdraw funds in the future when you’re in a lower tax rate. From a general standpoint, this advice holds but it misses a huge part of the equation for people who have the financial resources to maximize 401(k) plan contributions.

As addressed in the prior example, an $18,000 Roth 401(k) contribution is not equivalent to an $18,000 Traditional 401(k) contribution. The Traditional 401(k) amount has not yet been taxed which means that the IRS still owns a share of it. Specifically, a 60 year-old person in a 35% tax bracket with $18,000 in a Roth 401(k) can withdraw the entire $18,000 and spend it with no tax implications. Now assume the same conditions except that the $18,000 is in a Traditional 401(k). In this scenario, the person can withdraw the entire $18,000 but is only able to spend $11,700 because the IRS is owed the other $6,300 (35% x $18,000) by way of a deferred tax liability.

All of this is intended to demonstrate that while the contribution limits for Traditional and Roth accounts are the same in dollar terms ($18,000 or $24,000 if over 50), they’re not anywhere close to the same in terms of effective contribution limits. Because the Roth 401(k) uses after-tax dollars, it enables high income savers to effectively defer significantly more each year into a tax-friendly account.

The math on when it makes sense to use the Roth 401(k) option again relies on many assumptions which makes the analysis difficult when speaking in general terms. However, if we make reasonable portfolio tax efficiency assumptions Professionals and corporate executives nearing retirement can actually use the same framework as the mid-career professional above. One caveat is that the Roth 401(k) actually becomes less economically beneficial the closer someone gets to retirement because the important time variable shrinks (less time for tax-free compounding benefits to accrue). This does not mean that the Roth 401(k) tends to be a bad option for late career professionals. It just means that someone near retirement who anticipates a lower tax rate once they retire is often better using the Traditional 401(k) for savings. Again, the Roth or Traditional 401(k) question may seem trivial or just frustratingly complex so we created the framework above to help think about the decision at different stages of life. While we do not know what the tax code will look like in the future now nor do we know our personal income tax situation in 20 years, we can all make reasonable projections which then help to think through important decisions such as the Roth vs. Traditional 401(k) question. As we roll into a new calendar year where 401(k) deferrals begin anew, it is worth spending a few minutes on your own or with a financial planner to evaluate which of the Roth or Traditional 401(k) option makes the most financial sense. You’ll always have next week to decide on the old colleague’s Facebook friend request. What are your thoughts? Have questions on your specific situation or still don’t understand the decision framework? Leave your comments, questions, or ideas below. [i] For the table, we assumed that contribution limits start at $18,000 and increase by 3% per year. We also assume a 6% pre-tax rate of return and 20% combined capital gain/qualified dividend tax rate. To get a fair comparison, we create a side brokerage account for the annual tax savings created by the Traditional 401(k). In this side account, we assume 40% of gains are ordinary income, 15% qualified dividends, and 25% from realized gains each year. The analysis evaluates the net after-tax ending balance after 20 years of savings and growth.

Late-Career Professionals

Summary

[…] the Roth option exists, what percent of the deferrals should go to a Roth account versus a Traditional account? This is a ratio that should likely change as income increases or […]