Oxyphenbutazone is a non-steroidal, anti-inflammatory drug used mostly in eye-drops that was pulled from markets worldwide in the mid-1980’s for its link to bone marrow depression. More interestingly, but perhaps just as trivial, Oxyphenbutazone represents the highest possible scoring play in Scrabble. Play it across three triple word score squares and eight already-played, perfectly positioned tiles and you will earn a cool 1,778 points. Disappointingly, the probability of this play is so remote that experts agree the theoretical 1,778 points will almost certainly never be achieved in game play. But keep the word in mind the next time you’re playing Scrabble, the planets align, and unicorns are running through your back yard.

So what does Oxyphenbutazone and Scrabble tile scoring have to do with long-term investing? More than you might think. In fact, researchers at the Cass Business School in London uncovered a connection that might make Scrabble scoring the long sought Holy Grail of investing. Before we explain how Scrabble word scores could be the ticket to riches, we have to start with an explanation of how index funds like those based on the S&P 500 Index are constructed.

Scrabble Scoring as the Secret to Riches

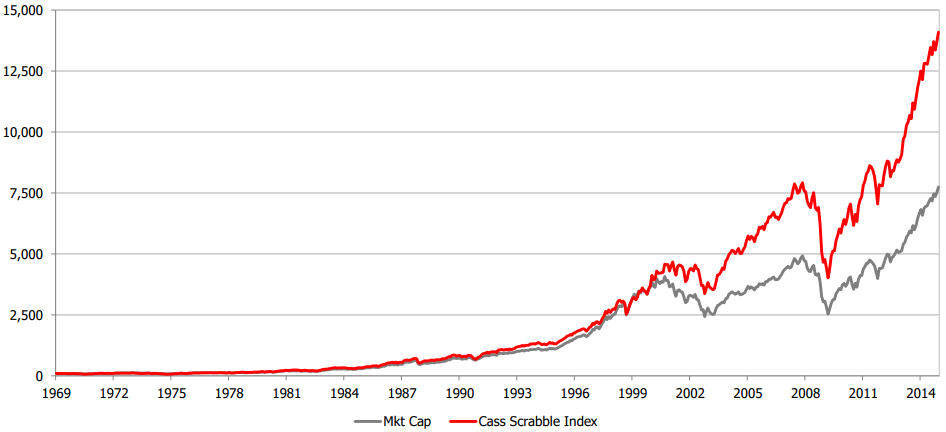

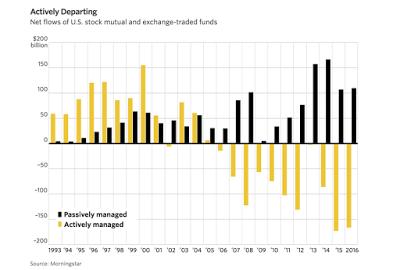

Far more important than deciding the stocks that go into an index or index fund is deciding how each of those stocks is weighted. Most indices such as the S&P 500 Index weight their constituent stocks based on the relative market value of the underlying companies. Market value, which is also called market capitalization (or market cap, for short), is simply the number of shares multiplied by the price per share. In the S&P 500, the companies with the largest market values such as Apple and Microsoft get the largest weights and smaller companies like Patterson Corp. get the smallest weights. Intuitively, this makes sense since the largest companies by market value should represent a larger piece of the economy. But researchers at the Cass Business School thought they could do better. Rather than use a measure such as market value to determine the weighting construction of an index, they opted to use Scrabble letter scoring. That is, they scored all the letters in each of the S&P 500 stock ticker symbols to quantify how each company should be weighted. Determine the score of each company’s ticker, add them up, and divide each company’s score by the total. Instead of Apple being the largest component based on its market value, the distinction in the new Scrabble 500 Index goes to Equinix where ticker EQIX scores 20 points. Companies like Agilent Technologies (ticker: A) and AT&T (ticker: T) score 1 point and get 1/20th the weight of Equinix. While the concept may sound preposterous, the results should get your attention. Over the lengthy 45 year period that the researchers tested, the Scrabble Index outperformed the S&P 500 by 1.53% per year. Keep in mind that most investment managers would trade the naming rights of their first born child for an extra 1.0% per year and this index outperformed by 1.5% per year. For 45 years. An initial investment of $10,000 in the S&P 500 in December 1968 appreciates to $771,800. The same investment in the theoretical Scrabble Index becomes $1,410,800 – $639k more than the S&P 500. So then the researchers test this Scrabble Index anomaly in other markets outside the US and it works with similar results – trouncing the relevant market capitalization benchmark. Even the risk-adjusted returns are notably better. Investing’s Holy Grail. Investors must just unknowingly gravitate to stocks with Q’s and Z’s in their ticker symbol. But the success does not stop here. Another research team experimented with indices designed by monkeys throwing darts. Actually, to avoid the time and cost required to have monkeys throw darts at the past 50 years of stock pages from the Wall Street Journal, they just simulate dart-throwing by randomly picking 30 stocks each year for 50 years and equally weighting the stocks. They run this simulation 100 times and the dart-throwing monkeys outperform in 96% of the 50-year trials. Similar to the Scrabble results, the monkeys added an average of 1.6% per year over the market capitalization-weighted index. This same team examined other index construction methodologies. Weight companies based on book value, on earnings, on the number of employees, on dividends, on free cash flow, on revenues – you get the idea. The more revenues or earnings or employees a company has, the larger its weight in the index. It hardly mattered what variation they used, the result was the same. Using any of these alternative weighting methodologies provided an additional 1% – 2.5% per year of additional return relative to the capitalization weighted indices such as the S&P 500. The results didn’t just hold true in the United States during a specific time period – they held true in all parts of the world over all kinds of different time periods. As opposed to the Scrabble and monkey throwing darts outcomes, there is at least some reasonable explanation for the results of these fundamental-weighting methodologies – investors get rewarded for owning more of the companies with higher earnings or higher sales. But the intriguing part is that when the researchers then used an inverse fundamental-weighting methodology – giving the highest weights to the companies with the smallest sales or the least profitable companies – the results were roughly the same. The new inverse-weighted indices also outperformed the capitalization weighted index over long time periods by 1.5% – 2.5% per year. While all these different weighting methodologies likely appear different, they all have one very important thing in common – they break the linkage between stock price and stock’s weight in the index. Remember again that the S&P 500 Index weights stocks based on market capitalization – number of shares times price per share. If a stock gets more expensive (the price of a stock goes up relative to other stocks), the stock automatically becomes a larger weight in the index. Consider the example of dot-com era darling, Cisco Systems. Cisco was added to the S&P 500 Index in December 1993 at which time it had a $6.9 billion market capitalization and represented a mere 0.15% of the Index. Over the next six years, Cisco’s stock price increased more than 4,000%. Since Cisco was appreciating at an enormous rate relative to other stocks, it’s weighting in the index also saw massive growth. By March 2000 in the height of the dot-com madness, Cisco became the largest company in the world as defined by market value with a $549 billion market value. It represented nearly 4.5% of the S&P 500 Index. You know how the story unfolds. The stock falls crashes 89% over the next 2.5 years. And this dramatic example helps explain the critical flaw in a market capitalization weighted index like the S&P 500. Importantly, every stock has an intrinsic value or fair value – how much the stock should be worth based on all its fundamentals and expectations. It is this fair value that individual and professional investors spend countless hours trying to determine and speculate on when they invest. The question for every company: is the current stock price above or below the intrinsic value? It is a mathematical truism than in a market capitalization weighted index like the S&P 500, every stock that is trading above its fair value gets a higher index weight than it should. Similarly, every stock that is cheap compared to its fair value gets underweighted. The bigger the error in the stock valuation – either a stock trading too cheap or too expensive – the bigger the overweighting or underweighting. Cisco represented roughly 0.02% of the economy according to fundamental measures but 4.5% of the index simply because investors bid the stock to egregious prices. All of the other index approaches we described before break that linkage between price and index weighting. In the Scrabble Index, Cisco (CSCO) represents ~0.2% of the index whether its stock price makes it a bubble or absurdly cheap. In an index based on a measure like revenues, number of employees, or cash flows – inverse or otherwise – its weighting in the index holds relatively still from month to month so as not to be impacted by stock price movement. The dart throwing monkeys also don’t overweight expensive stocks or underweight cheap stocks (at least we don’t think they do) – all the errors are random. That’s the key point. There will be errors in any index as expensive stocks are overweighted and cheap stocks are underweighted. The critical benefit of non capitalization-weighted indices is that they randomize these errors as opposed to always overweighting all expensive stocks and underweighting cheap stocks. Aside from stories about Scrabble and monkeys, we have spent all this time explaining index construction methodology and that may seem to have zero practical implications. “Why do I care how the S&P 500 Index is constructed?”, you might ask. In fact, the practical implications are enormous and literally impact trillions of dollars over the next decade. You may be aware that there has been a dramatic shift from actively managed investments to passively managed investments over the past decade. The evidence is depicted below. Although we do not dismiss some benefits of active management, we have been staunchly on the side of passive investments and remain firmly on that side in how we invest. We explain the rationale for this stance in this quarterly investment commentary. The vast majority out of the hundreds of billions of dollars flooding into passive investments has gone to funds that track market capitalization weighted indices like the S&P 500 or the Russell 2000. Our point here is not that the S&P 500 Index or other market cap indices are terribly flawed and should be avoided (although we have said that of the Dow Jones Industrial Average, which is a draconian accident of history). There are many positive features of the way these market cap indices are constructed. They tend to be more tax efficient and they are packaged by the likes of Vanguard, Schwab, and iShares in extremely low cost investment options. Instead, the practical point we hope to convey is that the construction of these market cap indices has legitimate flaws and that, resultantly, there may be a better way to passively invest[ii]. While we respect the merits of low-cost, cap-weighted indices and use them as part of our portfolio designs, we also contend that exclusively using these ultra-low cost market capitalization weighted investments in each asset class is not the ideal solution. We admittedly do not contend that monkeys throwing darts or indices constructed based on Scrabble scoring is the answer. However, it is our strong belief that passive funds (still low cost, just not the lowest cost) that break the direct linkage between price and weighting are likely to provide a better outcome. [i] An added benefit of this index methodology is that as a company’s stock price appreciates more than other companies, it automatically becomes a larger percentage of the index – no trading or rebalancing necessary. [ii] It should be noted that practitioners and academics married to the long-standing approach of capitalization-weighted indices often dismiss the results of the aforementioned research and data. The most prevalent objection to the findings (and we’re simplifying) is that any other index methodology besides capitalization weighting is active management. That is, if you’re not capitalization weighting an index, you’re making an “active bet.” We’re not going to get caught up in the semantics of defining active and passive management in this article but it is our belief that passive investing extends to index methodologies beyond just market capitalization weighting.

Why Do Dart Throwing Monkeys Almost Always Crush the S&P 500?

The Practical Implications

Hi Jason!

Hope this note finds you well and i appreciate the article(s).

I note the graph signals a change in returns beginning around 2004, or so. At that point we see returns from passive investing exceeding those from active investing. Any thoughts about why these profound changes began at that time?

Hi Max,

Glad you enjoyed the article. Admittedly, the chart you’re referencing lacks a label on the vertical axis but the dollars are fund flows (investment dollars) – not returns. That’s my fault for not labeling it better. What you’re seeing in the chart are the net dollars that have gone into active funds and passive funds each year. Active funds have clearly seen more redemptions than additions over the past decade. Much of this seems to be the result of individual investors recognizing that active funds tend to underperform passive funds over long-stretches because of increased competition, higher fees, and the difficult of differentiating skill from luck that we describe here: https://rpgplanner.com//luck-and-skill-in-baseball-and-investing/. Give me a call if you want to discuss further as I’d be happy to explain.