In a country founded on the idea of individual freedom, Americans value the idea of choice. We inherently believe that maximizing individual freedom increases our individual welfare or happiness and that the best way to maximize individual freedom is to maximize choice. A bar with 120 beers on tap is perceived better than a bar with two beers on tap. 36 varieties of chicken wings on a menu is perceived better than just a single offering of generic buffalo chicken wings. Anyone who has visited the grocery to grab something as simple as toothpaste or shampoo, though, recognizes the downside to choice!

We say we want choices but we sure do hate making them. When faced with more choices, we are less likely to make any decision – a phenomenon known as choice paralysis. In a famous experiment, two psychologists found that shoppers in the same store were 10 times more likely to purchase jam when faced with 6 varieties than when faced with 24 varieties. Exploiting this behavioral bias is one of the foundations of success for stores like Costco and Aldi with limited brand selection.

The 401k Rollover Dilemma

Most working Americans are confronted with a choice after they depart a job or retire: leave investments in an employer-sponsored retirement plan (i.e. 401k) or roll them into an IRA (free of any taxes). Many choose the path of least resistance in spite of the fact that the economically rational choice overwhelmingly tends to favor moving assets to an IRA.

Just as jam shoppers capitulated to choice paralysis when confronted with more jam options, research shows that 401k plan participants are more likely to participate in a plan with fewer choices than when there are many. If adding 50 more investment options to a 401k plan increases the likelihood that participants will not participate by 60%, imagine what happens if they are presented with tens of thousands of investment choices in an IRA. It is simpler for many to leave assets in a 401k, despite the drawbacks, as the choices are more limited and the decisions resultantly seem easier.

In fairness, many financial advisors promote IRA rollovers for the wrong reasons as they free up assets for product sales (annuities, commissioned investments, etc.). Consumers have good reason to be skeptical of this conflict laden advice. At Resource Planning Group, we do not sell any products and we are financially indifferent to assets held in a 401k or IRA. When we discuss this rollover decision, it is simply an evaluation of the benefits and drawbacks. The remainder of this posting contrasts the circumstances that favor leaving assets in a 401k or rolling them into an IRA.

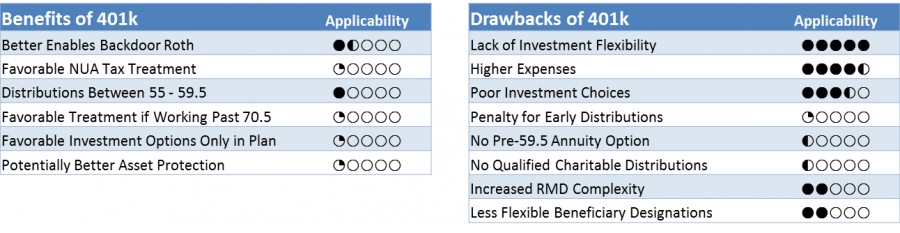

Potential Benefits of Keeping Assets in a 401k

- Better Enables Backdoor Roth IRA Contributions. In situations where you will be ineligible to make Roth IRA contributions in the future because of income limitations, keeping retirement assets out of a Traditional IRA is ideal. This benefit does not really apply to people who already have pre-tax IRA assets or who will still be eligible to make Roth contributions in the future. This posting explains the ins and outs of the backdoor Roth option.

- Favorable Tax Treatment for Employer Stock in 401k. If you own employer stock in a 401k with significant gains and have not yet reached age 59.5, it may be better to leave the 401k in place. The seldom used net unrealized appreciation (NUA) technique, if executed properly, allows employer stock in a retirement plan to be taxed at long-term capital gain rates instead of ordinary income tax rates. However, for many people, the tax impact of NUA is a penalty rather than a benefit. Most people would be well advised not to maintain employer stock in their 401k which is one of several reasons that this this benefit rarely materializes.

- Favorable Treatment if Retiring Between Ages 55 and 59 ½. Employees who retire after age 55 are able to take penalty-free distributions from a 401k – a luxury that is not afforded to IRA holders until age 59 ½. This benefit does not really apply if you retire after age 59 ½ or will not need to tap 401k assets before 59 ½.

- Favorable Tax Treatment if Working Beyond Age 72. If you plan to work beyond age 72 and you own less than 5% of the employer’s stock, you are permitted to defer required minimum distributions until your year of retirement.

- Investment Options Unavailable Outside the 401k. Some retirement plans, most notably the federal government’s Thrift Savings Plan, offer low cost investment options which are not available outside of the retirement plan. However, the overwhelming majority of plans either do not offer such options or, for those that do, the options are more costly than nearly identical investments outside of the plan.

- Potential for Better Asset Protection in Extreme Cases. Asset protection of IRAs is governed by state law whereas 401k plans and other qualified plans are covered by federal ERISA law. 401k plans are exempt from creditor claims under federal law. In contrast, some states do not exempt the full value of IRAs. For example, Georgia only protects the undistributed balance of IRA accounts under $1,245,000 outside of bankruptcy. If you have a 401k in excess of $1,000,000 and live in a state that does not fully exempt IRA assets from creditor claims, it may make sense to leave assets in the 401k if creditor protection is a concern.

Drawbacks of 401(k) Relative to an IRA

- Lack of Investment Flexibility. Most employer-sponsored 401k plans have limited investment options with between 5 and 50 choices. Alternatively, IRAs allow the purchase of nearly any stock, bond, mutual fund, exchange traded fund (ETF), real estate investment trust, or limited partnership – tens of thousands of investment choices. For investors who value choice, this is a dramatic difference between the two account types.

- High Expenses. 401k participants generally cover the financial burden of plan record keeping, administration, revenue sharing, and trustee costs. Although these expenses are now more transparent, most participants are unaware of the high 401k plan costs eroding their retirement savings. These expenses can and do cost mid-career professionals more than $100,000 over a working career. Rolling over assets to an IRA generally eliminates all of these plan administration costs, making the cost benefit of an IRA substantial.

- Poor Investment Choices. Not only are the investment options in a 401k limited, but to make matters worse, the limited investment options tend to be bad choices. Research shows that 401k plan trustees have an incentive to promote their own funds – a clear conflict of interest. Plans are resultantly littered with poor-quality funds. Using data from over 3,500 plans, recent research indicates that menu restrictions of poor fund choices results in an expected return reduction of 0.78% per year.

- 10% Penalty for Pre-59 ½ Distributions to Pay for Education Expenses, First-Time Home Purchase, and Other IRA Exceptions. The IRS provides several exceptions to the 10% penalty for distributions taken before 59 ½, but only for IRAs. These exceptions include first-time home purchases, qualified higher education expenses, and living expenses on account of disability. Distributions taken from a 401k to pay for such expenses before age 59 ½ incur a 10% penalty.

- No Annuity Option Before Age 59 ½. IRAs have a special option (IRC Section 72(t)) that permits penalty-free distributions before age 59 ½ using a series of substantially equal periodic payments. No such option exists for assets inside a 401k plan.

- No Qualified Charitable Distributions. The IRS permits IRA-account holders over age 72 to satisfy their required minimum distribution with a qualified charitable distribution (QCD). This favorable tax-saving option is not available for required distributions from 401k plans.

- Increased Complexity for Required Distributions. Once you reach age 72, the IRS requires you to take a minimum amount of annual distributions from your retirement accounts. In the case of IRAs, these distributions can be aggregated so that if you have multiple IRA accounts, you only need to take one distribution. In the case of 401k plans, required distributions cannot be aggregated so that you must take the calculated distribution from each plan. Moreover, Roth 401k accounts require these annual distributions whereas Roth IRA accounts do not – a meaningful benefit of Roth IRAs vs. Roth 401k plans.

- Less Flexible Beneficiary Designations. Most 401k plans will not accept customized beneficiary designations. In fact, all 401k plans require that a married plan participant name their spouse as 100% primary beneficiary unless the spouse signs off to permit other beneficiaries. IRAs do not require that a spouse be named as beneficiary and make it far easier to use customized beneficiaries.

Should I Rollover My 401k to an IRA?

As with nearly all financial planning decisions, the answer is: it depends. In most cases, the benefits of an IRA rollover overwhelm any benefits of leaving assets in a 401k. Simply quantifying the cumbersome 401k administrative expenses that can be completely avoided in an IRA provides ample justification for an IRA rollover. Generally, a departed employee has no desire to subsidize the high administrative costs and revenue sharing of his or her former employer. Limited low-cost investment choices in 401k plans tends to further justify a rollover in most cases. Alternatively, there are unique circumstances that favor leaving assets in a 401k plan so the answer for one person may not be the same answer for another person.

Although the 401k rollover decision requires making choices, it is not one that should be avoided or taken lightly. Whereas buying or not buying jam at the grocery store next week is a choice of little consequence in the grand scheme, the decision to leave assets in a 401k or move them to an IRA often has substantial implications.

Thoughts or questions? We would love to talk, connect with us!