Inflation is the sustained, upward movement of prices in an economy. It is not defined by the price changes of a single item, rather it measures the general trend of prices paid for a wide range of goods and services, reflected by an index like the Consumer Price Index (CPI). Generally speaking, prices for things like apparel and communication services tend to be more stable, while those of food and energy are more volatile, fluctuating regularly. While health care costs and college tuition have historically risen much faster than general inflation trends, prices for electronic devices like computers and televisions have normally fallen over time (while simultaneously witnessing significant performance improvements—a double win!) Thus, by looking at a large, diverse basket of goods and services over time, economists can get a sense for general inflation trends without getting overly focused on the occasional outliers that may capture the headlines on any given day.

The officials at the Federal Reserve (The Fed) who are responsible for setting monetary policy believe that long-term inflation in the range of ~2% per year is an ideal target. Why not 0%? The Fed operates under a “dual mandate” to support both maximum employment and price stability and has determined that an average 2% annual “headline inflation” is consistent with balancing these mandates. There are a few reasons for their reasoning. Firstly, interest rates tend to be related to inflation. Thus, a higher level of interest rates (usually associated with higher inflation) gives the Fed more room to cut rates to stimulate economic activity in the event of a recession. Secondly, maintaining positive inflation a bit above 0% provides an insurance buffer against deflation – the sustained downward movement in prices – which can be far more economically destructive than it may seem at face value.

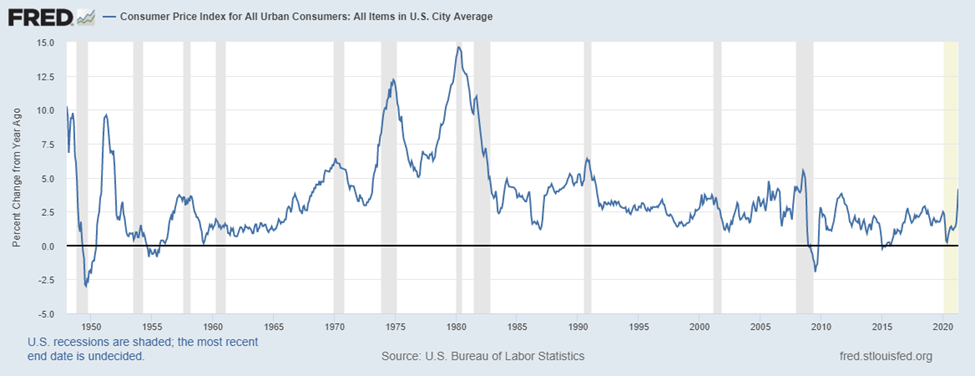

Following several years of below target price levels, inflation has recently found its way back to the front pages of the news. The combination of increasing demand from a sharply rebounding economy, combined with ongoing supply-chain challenges related to COVID-19, has created economy-wide supply/demand mismatches–a recipe for higher prices. Whether it be lumber used in home construction, semiconductors used in the manufacturing of increasingly advanced automobiles, oil, steel, or any related products; lately it seems that prices on just about everything are going up. Thus broad measures of inflation are rising, with the CPI recently registering its highest year-over-year increase since 2008.

As a hedge against rising prices, conventional wisdom tells us that traditional bonds are a poor investment choice. Since their fixed-coupon payments do not change over time, these bonds provide no purchasing power protection when inflation strikes. And with stocks being a higher-risk investment that may not align with an investor’s risk tolerance, a person might wonder what other lower-risk alternatives are available to protect their purchasing power. Enter Series I Government Bonds, an underappreciated savings vehicle designed to protect purchasing power from the destructive forces of rising prices.

I-Bonds are U.S. government savings bonds that earn a combined fixed interest rate plus a variable rate that periodically adjusts to changes in the Consumer Price Index (CPI). Thus, owners of I-Bonds receive an inflation protected return that also comes with several other attractive features, as well as a few caveats.

BENEFITS

- Safety of principal: I-Bonds are backed by the full faith and credit of the U.S. Government. As such, they are among the safest investments available, carrying virtually zero default risk.

- Protection against deflation: The opposite of inflation is deflation, a broad decline in price levels. Traditional bonds are a good investment choice in deflationary environments because they pay a fixed amount even when prices fall. Similarly, I-Bonds also provide deflation protection as they will never pay an interest rate below 0% and their redemption value can never decline. This makes I-Bonds an attractive alternative, even to TIPS (Treasury Inflation Protected Securities) which also provide an inflation hedge, but which can have negative price adjustments if deflation sets in after a period of inflation.

- Deferred taxes: Like all bonds issued by the Federal Government, the interest earned on I-Bonds is subject to federal income taxes, but is exempt from both state and local taxes, an advantage over savings accounts and CDs. However, unlike most government bond issues, the taxes owed on I-Bond interest can be deferred until they are redeemed or mature in 30 years, whichever comes first. As an example, this means I-Bonds could be purchased when a person is in their younger, income earning years while in a higher tax-bracket. However, the taxes owed could be deferred, possibly until retirement when the person may be in a lower tax bracket (possibly 0%).

- Potentially tax-free when used for education: Subject to certain criteria, if the proceeds of I-Bonds are used to pay for qualified education expenses in the same year they are redeemed, the tax bill can be avoided entirely. For taxpayers that meet these criteria, I-Bonds provide yet another tax advantage through tax-free growth.

- No transaction costs: I-Bonds can be purchased in virtually any denomination with zero commissions, markups or transaction costs. However, they must be purchased directly from the U.S. Treasury which means that your broker has neither the incentive nor the ability to purchase them for you. Admittedly, this creates a small, but easily surmountable hurdle in the purchase and redemption process.

POTENTIAL DRAWBACKS AND CAVEATS

As with most everything in life, nothing is perfect, and I-Bonds have certain features and caveats that you should be aware of before making a purchase.

- Lack of Marketability: I-Bonds are non-marketable and non-transferrable meaning they cannot be traded on an exchange and can only be redeemed by the original purchaser (however they can be given as gifts). They are intended to be a long-term savings and investment vehicle. As such, they are relatively illiquid investments that can only be redeemed via the Treasury or, in the case of paper bonds, at certain local financial institutions.

- Holding requirement – I-Bonds must be held for at least 12 months before they can be sold. Further, if they are sold within 5 years of issue, the holder must give up the last 3 months’ worth of interest.

- Relatively low rates of return: Given their high-degree of safety and security, the returns offered on I-Bonds are relatively low (the current fixed-rate portion is 0%). However, the benefits provided through inflation protection compensate for the low fixed-rate portion. To wit, in spite of the 0% fixed-rate, the current composite rate (fixed plus inflation component) is 3.54%.

- Limited purchase amount: While I-Bonds can be purchased in virtually any denomination, the purchaser is limited to a maximum purchase of $10,000/year per social security number. An additional $5,000 of paper I-Bonds can be purchased if done using a federal tax refund. By comparison, TIPS can be purchased in much larger amounts (up to $5 million).

- Interest is not received until redemption: Unlike traditional coupon bonds, I-Bonds do not send interest payments as an income stream, rather interest accrues over the life of the bond. I-Bonds are effectively “Zero-Coupon bonds”. That means interest payments are added to the value of the bond and ultimately collected when the bonds are redeemed at face-value plus accrued interest.

If you’d like more information about I-Bonds or are interested in making a purchase, we encourage you to visit TreasuryDirect.gov to learn more. Click here to learn more about Treasury Inflation Protected Securities (TIPS), and how they help hedge against inflation risks.

To understand how we help clients navigate inflation over the long-term through Planning Right, give us a call! You can click here to schedule an Introductory Call with one of our advisors to discuss the long-term impact inflation can have on your financial security.

Leave A Comment