Last Friday here in Atlanta, local businesses closed, restaurants shut their doors by late afternoon, school activities were cancelled, and the Atlanta metro region went under a State of Emergency in anticipation of a debilitating storm. Meteorologists unanimously predicted 2-5 inches of snowfall later that evening – an obviously dire amount of snowfall by southern standards.

Atlanta’s youth awoke Saturday morning with Christmas morning excitement and plans to build snowmen or go sledding. Instead, they were met with the same disappointment that has befallen many young Atlantans before them – only a small coating of ice and bone-chilling temperatures. No snowmen. No snow ball fights. No snow angels.

Admittedly, weather forecasters do not have an easy job. They are expected to make predictions about the future and they are often wrong in an imperfect science. Sometimes, like last week, they are very wrong (of course, the same could be said for political pollsters) and society is still collectively disappointed and bewildered by their inability to accurately predict the future.

Unlike meteorologists, we do not make predictions or forecasts about the future. Whereas there is a mystique and an emotional appeal for prediction-making in financial markets, we believe that it is a horribly flawed exercise that better serves short-term sales targets than productive good for clients. Trying to prognosticate and time financial markets is exciting but financially destructive – a topic that we have explained in many prior commentaries (see here, here, and here).

We are planners, not prognosticators. Likewise, we firmly believe that our highest value services for you, our client, are to plan for all potential outcomes, simplify your financial life, align portfolios and planning advice with your long term goals, and to educate you so as to help make wise financial decisions and to avoid overreaction to market events.

It is that last point that we choose to cover here – helping you to make sense of what’s happening in this wild and fast moving world and what it means to financial markets. Although we could cover dozens of topics and events that impacted markets in 2016 or may impact markets in the future, we choose four below to highlight and explain, starting with the post-election stock rally.

The Trump Bump

US stocks were flat in 2016 after an 8-day losing streak in the 4th quarter that marked the longest skid since 2008. Then came a surprise election result. Next came a surge in domestic stocks that left the S&P 500 up 12% for the year.

This “Trump Bump” for stocks has been fueled by an anticipation of pro-business policies of President-elect Trump and the Republican-controlled Congress. The expectation of looser industry regulation, fiscal stimuli, tax cuts, a tax holiday for foreign profit repatriation, and a business-friendly administration all gave hope to a surge in business and investor confidence which, in turn, helped lift stocks. All of these policies are likely positive for growth in the short run. It also did not hurt that corporate profits rebounded in the 2nd half of 2016, oil prices recovered dramatically after falling below $30/barrel in early 2016, and employment markets continued to improve.

History demonstrates that the President of the U.S. is not as important to financial markets as people tend to believe. Yet this does not stop emotion from causing investors to overreact in both directions. It is important for both sides of the partisan divide to remember that the long-term implications of Trump policies are unclear – just as they are for any president – and that there is still uncertainty as to what campaign promises will be realized. Moreover, we also remind our readers that there is a behavioral tendency for supporters of the losing party to invest more conservatively while their party is out of power and resultantly experience worse investment returns.

Interest Rates and Inflation

In contrast to stocks, the implications of Trump policy are almost polar opposites for the bond market. Specifically, if you were to draft an economic playbook on how to generate inflation using fiscal policy, it would begin with the following plays:

- Spend significantly on debt-financed, productive infrastructure (because unproductive infrastructure spending like building roads to nowhere is not inflationary).

- Erect trade barriers (tariffs, quotas) thereby reducing the supply of cheap goods or raw materials.

- Restrict the supply of cheap labor by increasing minimum wage and/or limiting the supply of low skilled immigrants.

- Enact significant tax cuts which encourage consumer spending and increase budget deficits.

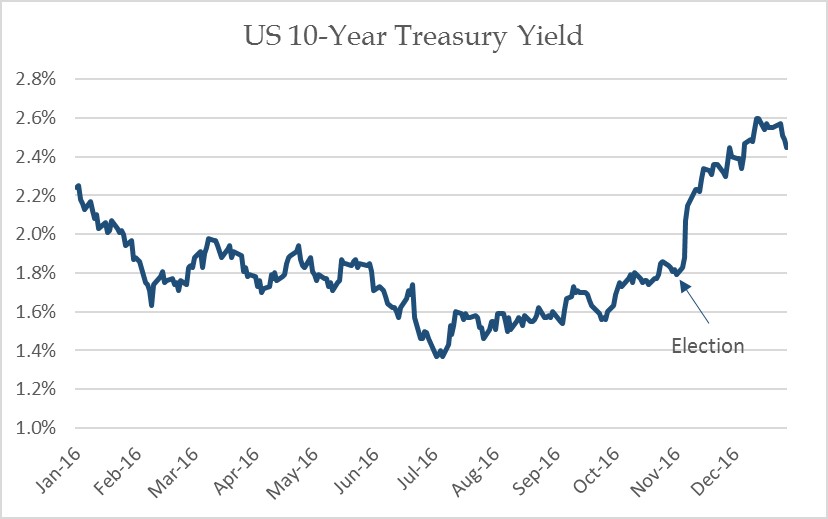

Clearly to anyone who followed the election, this economic playbook matches closely with the policy prescriptions of President-elect Trump. Given that inflation expectations have a direct impact on long-term interest rates, it should be no surprise that inflation expectations surged and long-term interest rates experienced a historic increase immediately following the election results. 10 -Year US Treasury yields moved from 1.8% to over 2.5% – the largest 20-day spike in rates since World War II.

-Year US Treasury yields moved from 1.8% to over 2.5% – the largest 20-day spike in rates since World War II.

What does this mean for bond investors? It means that most bond categories and other high income assets experienced declines in November and December because of the increase in rates. However, we do not believe that it should be a reason to exit bonds. The reality is that bonds now provide significantly higher nominal return expectations than they did a few months ago which, all else equal, makes them more attractive relative to other investments – not less attractive.

Are Stocks Cheap or Expensive?

Seemingly sophisticated financial experts love to talk about economic growth, GDP data, employment gains, housing starts, and a bevy of other backward-looking economic data as if these things matter most to investors. We again issue the important public service reminder that Main Street does not equal Wall Street.

To be fair, there is a correlation between economic growth and stock returns. It’s negative. Empirical data demonstrates that the lower a country’s economic growth, the higher that country’s stock market return is. Likewise, countries with high economic growth experience lower stock market returns. The same empirical evidence holds for individual stocks – the higher the growth, the lower the future return.

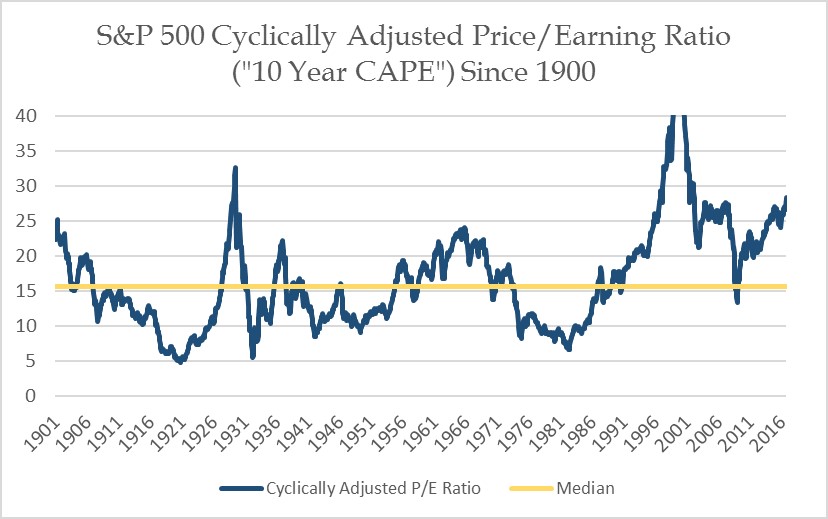

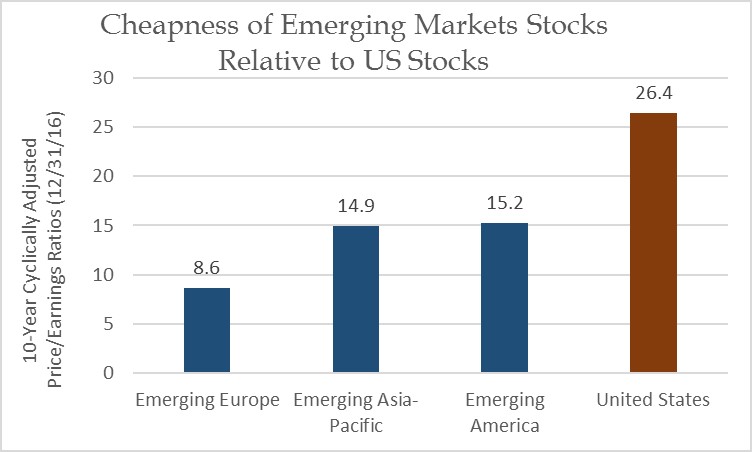

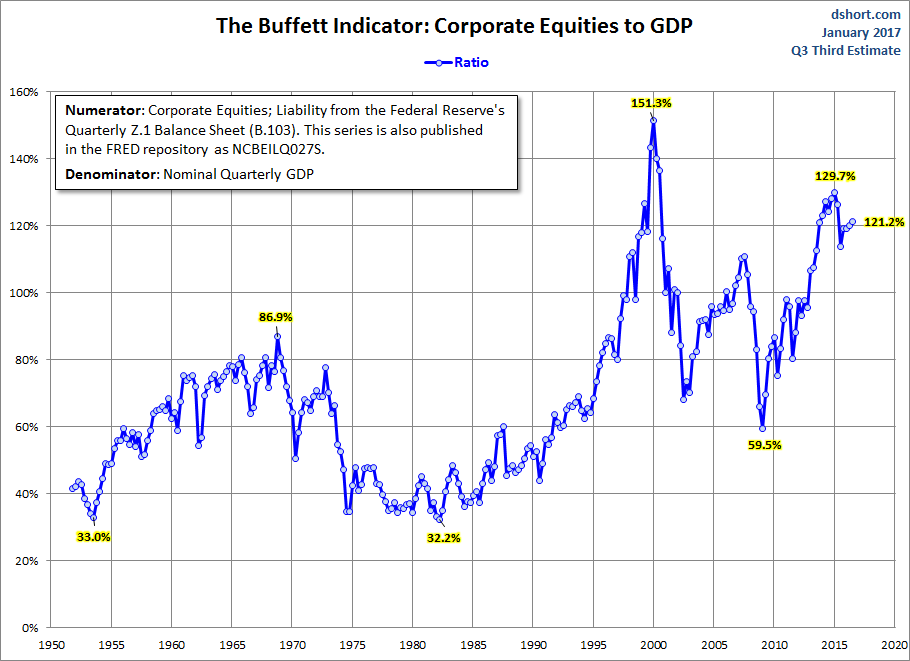

This “growth paradox” is largely explained by the role of valuation. High growth assets, countries, sectors, or stocks tend to have expensive prices which imply lofty expectations. When these So where are valuations today? Following eight consecutive positive calendar years, stocks in the United States are expensive. Keep in mind that there is no perfect way to assess valuations but nearly all useful measures are at elevated levels. You can click here to view Warren Buffet’s favorite measure of valuation or here to view the Fed’s favorite model – both of which depict historically rich levels. We highlight (in the adjacent cha This is not to say that investors should avoid owning stocks. First, while valuations are a useful predictor of long-term returns, they are fairly awful as a short-term indicator. Second, high valuations do not imply a market correction – they simply imply lower long-term expected returns – expected returns that still exceed cash and bonds. Lastly, these elevated valuations are largely endemic of US stocks whereas foreign stocks look somewhere between reasonably priced and cheap. After several years of lackluster returns, emerging market stocks were on pace for a redemption year in 2016. Through the end of October, the MSCI Emerging Markets Index was up 16.3% – more than 10% better than large cap US stocks. Again, the US election quickly changed things – in this case, reversing the performance advantage of emerging market stocks so that US stocks outpaced for a 4th straight calendar year. On the surface, Trump policy is almost universally unfavorable for emerging markets. Protectionist trade barriers are clearly negative for foreign countries like China and Mexico that export goods to the United States. Additionally, the inflationary policies that caused US a dramatic rise in US interest rates following the election present significant headwinds for emerging markets. The higher US interest rates attract capital out of emerging market investments, thereby reducing the value of the local currency. Not only are emerging market investments hurt by the weaker currencies but the dollar-denominated debt of emerging market borrowers becomes harder to pay off. So what does this mean for investors? We first point out that while a stronger US dollar hurts emerging markets in the short-run, it has a positive long-term benefit. The stronger dollar makes foreign goods and services cheaper for US consumers which makes these emerging market exporters more competitive in the long run. Secondly, we point again to the valuation topic as valuation levels are much more favorable for emerging market stocks than they are for domestic stocks. These attractive valuations suggest that forward-looking return expectations for emerging market stocks are significantly higher over extended time periods. Importantly, these valuation discrepancies tend not to be useful for short-term predictions but quite helpful at predicting long-term outcomes. The reality is that our brains cause us to think we know more than we do, to think we’re better investors than everyone else, and to think we can forecast the future. Yet most times, as we’ve highlighted above, there are two sides to a coin. Don’t believe everything you read or hear without understanding the other side. We do not aspire to be weather forecasters, pollsters, or market prognosticators. We are planners. Part of that planner role is understanding current market dynamics to help make wise investment and financial planning decisions for the long-term. Another part of the role is helping explain and decipher those market dynamics to you so that you can better make sense of things. We hope that this has helped in that respect and welcome any questions you might have about investments, finances, or your retirement plan. rt) our preferred measure, the cyclically adjusted P/E ratio or “CAPE”.

rt) our preferred measure, the cyclically adjusted P/E ratio or “CAPE”.What’s Going on with Emerging Markets?

What It All Means to You

{kind=link}

Fine explanation of a complex subject. And with an enjoyable touch of humor. It’s understood that you can not and should not predict the economy’s future. Knowing little about all this, my ignorance is not so constrained. I’m expecting whiplash to become a constant companion as the US makes many very surprising political moves.

Thanks for the kind words and the support, Bob.